Tax Form 8949 Instructions for Reporting Capital Gains and Losses

Keeping up on the changes made by the IRS can be tricky. If you have capital gains or losses, then they must be reported on your taxes. Changes in the reporting process were made a few years ago, that you need to be aware of. You may need to use Form 8949 addition to totaling up your transactions on the previously used Schedule D only. Completing Form 8949 is a bit complicated, but if you’re organized, it will make things go faster.

Description of Capital Gains and Losses

If you’re unfamiliar with these terms, here is how to know if they apply to you. Whenever a capital asset is sold, this generates a capital gain when profit is made on the transaction, but if you lose money, it becomes a capital loss. A capital asset is anything that you own. The list includes vehicles, stocks, collectibles and all other possessions.

What the IRS requires from you

You are required to report the income that you make from all capital gains. The total figure for the year is needed to determine the right amount of income tax. In some cases, when there is a capital loss, you can take a tax deduction. Not every capital loss qualifies for a deduction though. For example, if you sell your home and take a loss, this does not qualify for a tax credit, but you can take the credit if you lose money on the sale of stocks.

Two kinds of Capital gains and losses

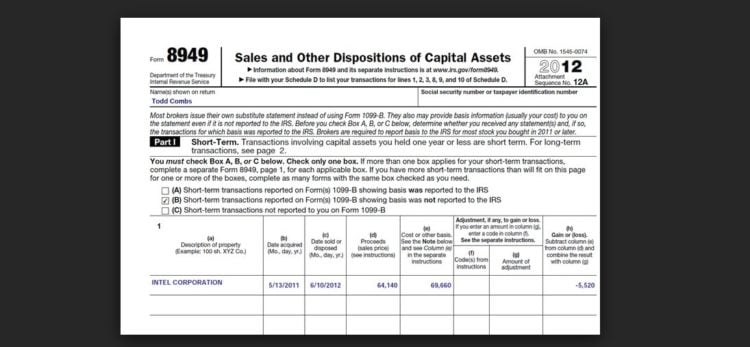

There are two varieties of capital gains and losses. These are short term, and long term. A short term refers to something that you owned for less than one year, and long term is something that you owned for more than a year. For example, if you owned stocks for 6 months and sold them, taking a loss, this would be considered a short term capital loss. If you made a profit on the sale, it would be a short term capital gain.

Dealing with stocks, bonds and mutual funds

The price that you paid for an item, such as stocks, bonds and mutual funds is called the Basis. Your stock broker can assist you in determining gains or losses, which are reported on your 1099-B Form. You might have received assets that do not have the basis reported on the 1099-B Form. If this is the case, you must go through your records to figure out the basis amount (amount you paid), and do the calculations to determine whether the sale resulted in a gain or a loss. When some assets have the basis reported on the 1099-B Form, and others do not, you might need to file more than one 8949 Form.

Not everyone needs to file the Form 8949

If your 1099-B Form lists all assets for which capital losses or gains are realized, and includes the correct basis, and if it turns out that there are no adjustments that need to be entered on column g, and no codes in column f, then you won’t need to file the Form 8949, but will are still required to file Schedule D.

8949 tax form looks complicated but it doesn’t need to be

The most difficult part of completing this form is arriving at the correct basis, and determining the capital gains and losses from sold assets. If you have all your information available, the process goes more quickly and it’s just a matter of doing simple math to find out if you made money or lost money on each asset. It gets more complicated when there are several sold assets to calculate.

How to calculate capital gains/losses

Prior to completing the forms, list all gains and losses for the year. Match the 1099-B for each transaction. Divide the transactions into six different groups.

- Long term transactions reported on a 1099-B with basis reported to the IRS

- Long term transaction reported on a 1099-B with basis NOT reported to the IRS

- Long term transactions that do not have a 1099-B Form

- Short term transactions reported on a 1099-B with basis reported to the IRS

- Short term transaction reported on a 1099-B with basis NOT reported to the IRS

- Short term transactions that do not have a 1099-B Form

Situations

When all your transactions were reported on a 1099-B Form and none require the recording of any codes or adjustments, and all include the basis, you may report the total of the transactions on the Schedule D and you DO NOT need to file Form 8949.

When you are required to report short term transactions on page one of Form 8949 and long term transactions on page two, you will need to complete a separate Form 8949 if you have additional transactions that fall into a different category.

What if all but one short term transactions list the basis?

In this case, you are required to complete a separate 8949 Form for the transactions that did not report the basis. If there are several, you may need to complete several Form 8949 for filing. This is why it’s important to organize all your information prior to starting.

Information required for Form 8949

For each transaction, you will need the following pieces of information to complete the Form

- The date of purchase or acquisition

- The Date sold

- The sale amount

- Cost or Other Basis, which is the amount paid for the asset, plus fees or commissions if applicable.

- Any 1099-B forms for the transactions, if basis is listed on this form use that figure.

- If the asset is from an inheritance, the value of the asset at the time the person passed away is used.

- Any special codes. For example, the code for Wash sales is a W in column f, any nondeductible parts of a wash sale go in column g, and if the basis is incorrectly reported on thee 1099-B, a Code B is required.

Although Form 8949 looks complicated, if you have your information and documentation well organized, it’s not that difficult to complete. If you’re unsure of doing the process yourself, you can seek the assistance of a reputable tax preparer to assist you with the process.